The Milliman Mortgage Default Index (MMDI) is a lifetime default rate estimate calculated at the loan level for a portfolio of single-family mortgages. For the purposes of this index, default is defined as a loan that becomes 180 days or more delinquent.1 The results of the MMDI reflect the most recent data acquisition available from Freddie Mac, Fannie Mae, and Ginnie Mae, with measurement dates starting from January 1, 2014.

Key findings

As interest rates rose in the second quarter (Q2) of 2021, total mortgage originations declined. Purchase originations remained strong, but refinance activity decreased by approximately 30% quarter-over-quarter. This decrease has implications for the average default rate for new originations as refinance loans (when they are rate/term refinances) tend to have lower risk profiles relative to purchase originations.

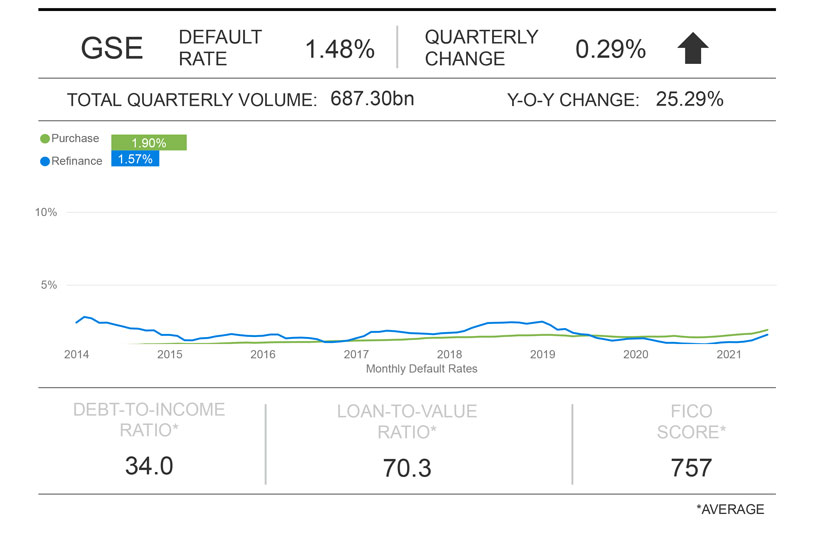

Largely driven by the decrease in refinance loans, the total default risk quarter-over-quarter for government-sponsored enterprise (GSE) acquisitions during Q2 2021—loans acquired by Freddie Mac and Fannie Mae—increased 1.48% for loans originated in Q2 2021 compared to the 1.20% increase for loans originated in Q1 2021. Figure 1 provides the quarter-end index results for these loans segmented by purchase and refinance.

FIGURE 1: MMDI 2021 Q1 DASHBOARD FOR GSE LOANS

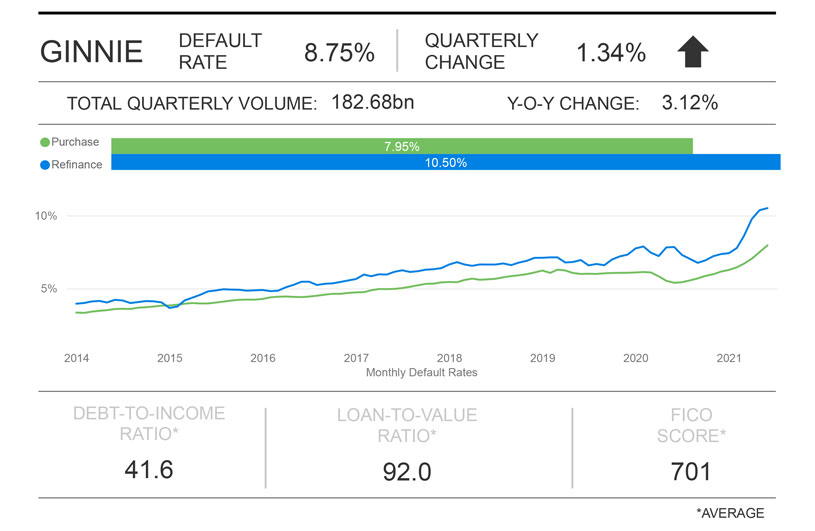

The MMDI for Ginnie Mae loans increased from 7.41% in Q1 2021 to 8.75% in Q2 2021, as can be seen in Figure 2 (segmented by purchase and refinance). For certain types of refinance loans (i.e., streamlined refinance loans), Ginnie Mae acquisitions do not receive an updated credit score. For the MMDI, a credit score of 600 is conservatively used to calculate the default risk on mortgages with missing credit scores. Because a large portion of volume was refinance volume, many Ginnie Mae loans are getting assigned a low credit score of 600.

FIGURE 2: MMDI 2021 Q1 DASHBOARD FOR GINNIE LOANS

When reviewing quarter-over-quarter changes in the MMDI, it is important to note that the Q1 2021 MMDI values for GSE and Ginnie Mae acquisitions have been restated since the last publication, changing from 1.52% to 1.20% and 9.30% to 7.41%, respectively. This is a result of updating actual home price movements from forecasted values and updating home price appreciation forecasts with the most recent forecasts available.

Agency summary

Interact with the MMDI

To explore the MMDI data on a more granular level, including loan origination and type, click here.

Consistent with the prior quarter, there has been an increase in the default risk for Freddie Mac and Fannie Mae acquisitions compared to the prior quarter. All three risk components in the MMDI contributed to an increase in overall default risk, with higher emphasis on borrower and economic risk. Loans guaranteed by Ginnie Mae experienced an increase in their default risks in Q2 2021 relative to the prior quarter as well.

Components of Default Risk

The components of the MMDI that inform default risk are borrower risk, underwriting risk, and economic risk. Borrower risk measures the risk of the loan defaulting due to borrower credit quality, initial equity position, and debt-to-income ratio. Underwriting risk measures the risk of the loan defaulting due to mortgage product features such as amortization type, occupancy status, and other factors. Economic risk measures the risk of the loan defaulting due to historical and forecasted economic conditions.

BORROWER RISK RESULTS: Q2 2021

For GSE loans, borrower risk increased from 1.03% in Q1 2021 to 1.17% in Q2 2021. The main driver of the increase is the combination of lower average credit scores and slightly higher loan-to-value ratios. For Ginnie Mae loans, borrower risk increased in Q2 2021 relative to Q1 2020 from an average of 6.11% to 6.47%. Ginnie Mae loans generally have a lower credit score and higher loan-to-value ratio.

UNDERWRITING RISK RESULTS: Q2 2021

Underwriting risk represents additional risk adjustments for property and loan characteristics such as occupancy status, amortization type, documentation types, loan term, and others. Underwriting risk after the global financial crisis remains low and is negative for purchase mortgages, which were generally full-documentation, fully amortizing loans.

ECONOMIC RISK RESULTS: Q2 2021

Economic risk is measured by looking at historical and forecasted home prices. Actual home price appreciation has been robust from 2014 through 2021, which has resulted in embedded appreciation for older originations. This results in reduced default risk for older cohorts. For more recent cohorts, we anticipate slower home price growth (or negative growth for some local geographies) after housing supply returns post-pandemic, which contributes to increases in economic risk for recent origination years.

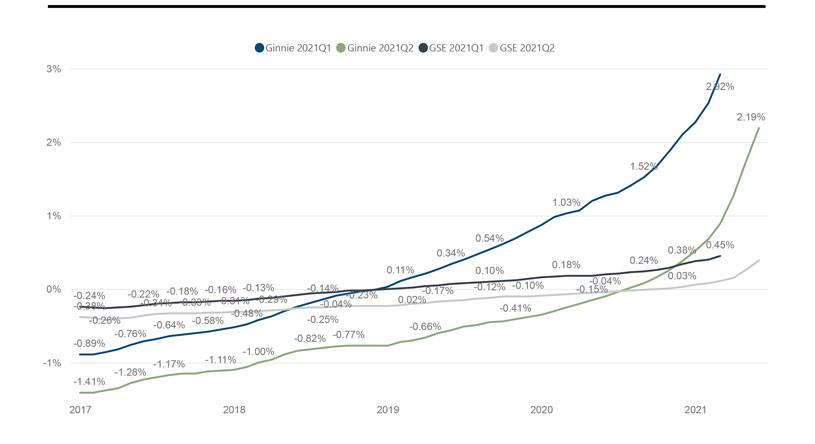

Figure 3 shows the economic risk component of the MMDI for Ginnie Mae mortgages and GSE mortgages stated as of Q1 2021 and Q2 2021. We notice from the chart that economic risk has remained steady for older originations, while economic risk for newer originations has sharply increased as we expect a slowing of home price appreciation in the future. However, in the Q2 2021 release economic risk decreased quarter over quarter (i.e., the lines in the chart for the Q2 2021 release are lower relative to the Q1 2021 release). This is because actual home price movements were more favorable than previously forecasted.

FIGURE 3: ECONOMIC RISK BY INVESTOR AND ORIGINATION

While the current level of robust home price growth is certainly a function of the pandemic and supply/demand imbalances, it is difficult to estimate how home prices may react post-pandemic. The MMDI reflects a baseline forecast of future home prices. To the extent actual or baseline forecasts diverge from the current forecast, future publications of the MMDI will change accordingly. Please read the disclaimer for COVID-19 for more context on economic risk.

For more detail on the MMDI components of risk, visit milliman.com/MMDI.

COVID-19 effects on mortgage risk

Significant uncertainty continues regarding how mortgage performance may be affected by the COVID-19 pandemic and its associated economic impacts. While unemployment rates, delinquency rates, and the percentage of loans in forbearance have increased rapidly since the start of the pandemic (and remain at elevated levels), the housing market has remained resilient. Please refer to prior releases of the MMDI,2 as well as a recent Milliman article on the topic3, for more detailed discussions of the potential impact of the pandemic on mortgage performance.

About the Milliman Mortgage Default Index

Milliman is expert in analyzing complex data and building econometric models that are transparent, intuitive, and informative. We have used our expertise to assist multiple clients in developing econometric models for evaluating mortgage risk both at the point of sale and for seasoned mortgages.

The Milliman Mortgage Default Index (MMDI) uses econometric modeling to develop a dynamic model that is used by clients in multiple ways, including analyzing, monitoring, and ranking the credit quality of new production, allocating servicing sources, and developing underwriting guidelines and pricing. Because the MMDI produces a lifetime default rate estimate at the loan level, it is used by clients as a benchmarking tool in origination and servicing. The MMDI is constructed by combining three important components of mortgage risk: borrower credit quality, underwriting characteristics of the mortgage, and the economic environment presented to the mortgage. The MMDI uses a robust data set of over 30 million mortgage loans, which is updated frequently to ensure it maintains the highest level of accuracy.

Milliman is one of the largest independent consulting firms in the world and has pioneered strategies, tools, and solutions worldwide. We are recognized leaders in the markets we serve. Milliman insight reaches across global boundaries, offering specialized consulting services in mortgage banking, employee benefits, healthcare, life insurance and financial services, and property and casualty insurance. Within these sectors, Milliman consultants serve a wide range of current and emerging markets. Clients know they can depend on us as industry experts, trusted advisers, and creative problem-solvers.

Milliman's Mortgage Practice in Milwaukee is dedicated to providing strategic, quantitative, and other consulting services to leading organizations in the mortgage banking industry. Past and current clients include many of the nation's largest banks, private mortgage guaranty insurers, financial guaranty insurers, institutional investors, and governmental organizations.

1For example, if the MMDI is 10%, then we expect 10% of the mortgages originated in that month to have become 180 days or more delinquent over their lifetimes.

2The MMDI report on 2019 Q2, for example, is available at https://us.milliman.com/en/insight/mortgage-default-index-2019-q2.